Understanding home valuation is crucial whether you’re refinancing your mortgage, selling your property, or just curious about your home’s worth. An appraisal is a professional assessment of a property’s market value, conducted by a licensed appraiser, and it plays a pivotal role in real estate transactions. For homeowners, knowing how appraisals work can save time, money, and stress. In this guide, we’ll dive into the essentials, including how long an appraisal remains valid, the specifics of refinancing, and unique considerations for mobile homes. By mastering these basics, you’ll be better equipped to navigate the real estate landscape with confidence.

A home appraisal is typically valid for 90 to 120 days, but this can vary based on lender policies and market conditions. For refinancing, lenders often require a recent appraisal to ensure the property’s value supports the loan amount.

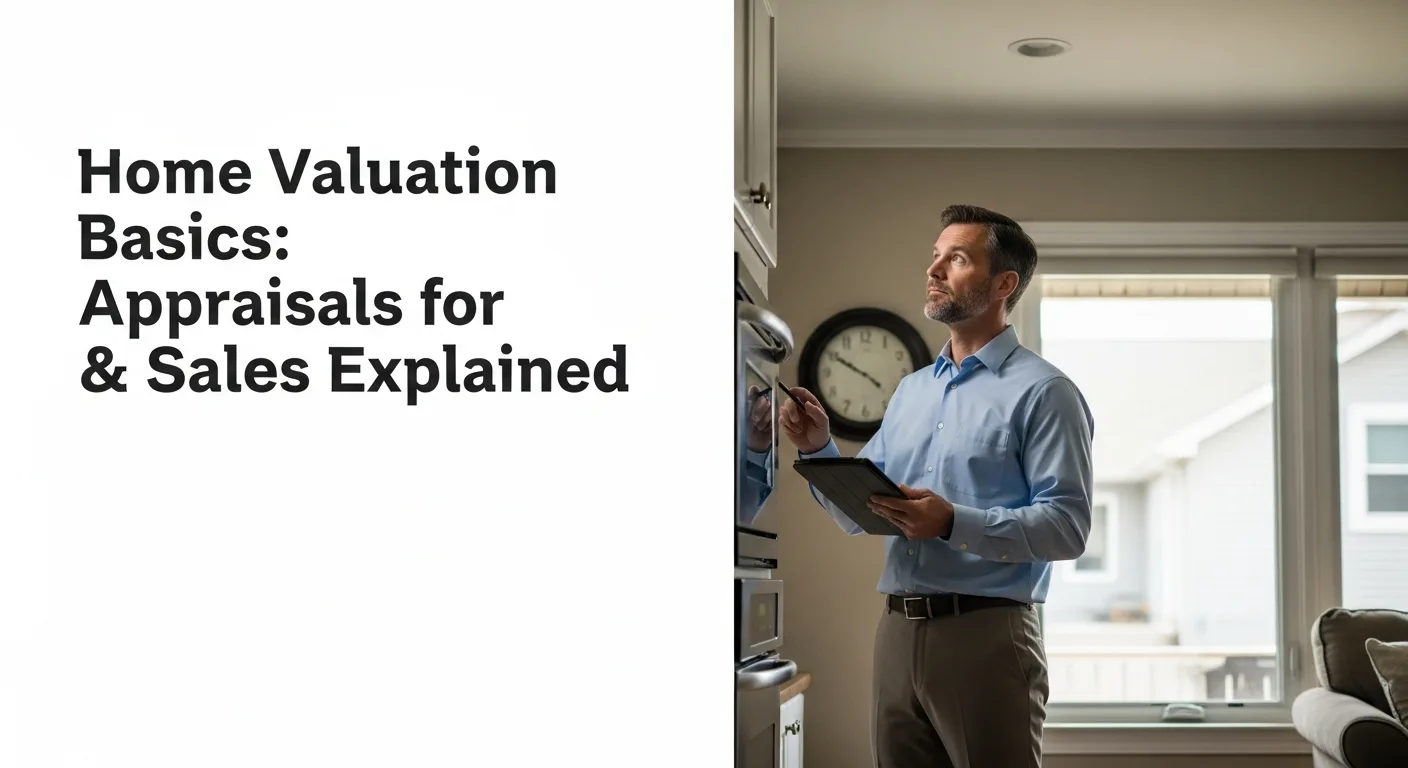

How Long Is a Home Appraisal Good For?

The validity period of a home appraisal is a common question among homeowners. Generally, an appraisal is considered current for 90 to 120 days from the date it’s completed. This timeframe is standard because real estate markets can fluctuate, and lenders want to ensure the valuation reflects current conditions. However, several factors can influence this duration:

- Lender Requirements: Different banks or mortgage companies may have specific policies. Some might accept an appraisal up to 6 months old if market conditions are stable, while others insist on a new one after 90 days.

- Market Volatility: In rapidly changing markets, appraisals can become outdated quicker. If home prices are rising or falling sharply, lenders may require a more recent assessment.

- Property Changes: Any significant alterations to the home, such as renovations or damage, can void an old appraisal. For example, if you’ve upgraded your kitchen or added a room, a new appraisal is necessary to capture the increased value.

It’s essential to check with your lender or real estate agent to confirm their specific guidelines. For those planning to sell or refinance, timing your appraisal strategically can help avoid delays. If you’re considering home electrical upgrades, these improvements might boost your home’s value and warrant a fresh appraisal.

Home Appraisal for Refinance: What You Need to Know

When refinancing your mortgage, an appraisal is often required to determine the current market value of your home. This ensures the loan amount doesn’t exceed the property’s worth, protecting the lender’s investment. Here’s a breakdown of key points:

- Purpose: The appraisal helps lenders assess risk and set loan terms. If your home’s value has increased, you might qualify for better rates or cash-out options.

- Process: An appraiser will visit your home, inspect its condition, and compare it to similar properties recently sold in your area. They’ll consider factors like square footage, age, and amenities.

- Costs: Appraisal fees typically range from $300 to $500, but this can vary by location and property type. These costs are usually paid by the homeowner as part of the refinancing process.

To prepare for a refinance appraisal, ensure your home is in good condition. Minor repairs and decluttering can make a positive impression. Additionally, understanding home security upgrades might add value, as safety features are often appealing to appraisers.

Selling a Mobile Home: Valuation and Appraisal Tips

Selling a mobile home involves unique valuation challenges compared to traditional houses. Mobile homes, also known as manufactured homes, require specialized appraisal methods. Here are some tips to navigate this process:

- Use the Mobile Home Blue Book: Similar to car valuations, the Mobile Home Blue Book provides estimated values based on make, model, age, and condition. It’s a useful starting point, but it’s not a substitute for a professional appraisal.

- Hire a Specialized Appraiser: Look for appraisers experienced with manufactured homes. They’ll understand factors like HUD certification, foundation type, and park fees, which can significantly impact value.

- Consider Location: Whether your mobile home is on private land or in a park affects its value. Homes in well-maintained communities with amenities tend to appraise higher.

For sellers, investing in mobile home skirting or other upgrades can enhance curb appeal and potentially increase the appraisal value. It’s also wise to review mobile home foundation options to ensure stability, which appraisers note positively.

Key Factors That Influence Home Appraisal Values

Appraisers evaluate multiple elements to determine a home’s worth. Understanding these factors can help you maximize your property’s value. Here’s a table comparing common appraisal considerations:

| Factor | Description | Impact on Value |

|---|---|---|

| Location | Proximity to schools, amenities, and low crime rates | High – prime locations boost value significantly |

| Condition | Overall maintenance, age of systems (e.g., roof, HVAC) | High – well-kept homes appraise higher |

| Square Footage | Total livable space, including finished basements | Moderate – larger homes generally have higher values |

| Comparable Sales | Recent sales of similar homes in the area | High – appraisers rely heavily on comps |

| Upgrades | Renovations like kitchen remodels or energy-efficient features | Moderate to High – quality upgrades can increase value |

To improve your appraisal outcome, focus on areas with the highest impact. For instance, ensuring your home water treatment system is up-to-date can appeal to appraisers looking for modern amenities.

Steps to Prepare for a Home Appraisal

Proper preparation can lead to a more favorable appraisal. Follow these steps to get ready:

- Clean and Declutter: A tidy home makes a good impression and allows the appraiser to see all features clearly.

- Complete Minor Repairs: Fix leaky faucets, broken windows, or peeling paint. These small issues can negatively affect the appraisal.

- Gather Documentation: Have records of recent upgrades, permits, and maintenance ready to share with the appraiser.

- Highlight Improvements: Point out any new installations, such as updated appliances or security systems, during the inspection.

If you’re planning to set up a home gym, consider how this addition might be viewed—it could add functional space that appeals to buyers and appraisers alike.

Frequently Asked Questions (FAQs)

How long is a home appraisal good for when selling?

When selling a home, an appraisal is typically valid for 90 to 120 days, similar to refinancing. However, if the sale process extends beyond this period, the buyer’s lender may require a new appraisal to ensure the value hasn’t changed.

Can I use an old appraisal for refinancing?

It depends on the lender and how old the appraisal is. Most lenders prefer appraisals less than 90 days old, but in stable markets, they might accept one up to 6 months old. Always check with your specific lender for their policies.

What is the Mobile Home Blue Book?

The Mobile Home Blue Book is a valuation guide that provides estimated prices for manufactured homes based on factors like age, model, and condition. It’s a useful tool for getting a rough idea of value, but for official transactions, a professional appraisal is recommended.

How does a home appraisal affect refinance rates?

A higher appraisal value can lead to better refinance rates because it lowers the loan-to-value ratio, reducing the lender’s risk. Conversely, a low appraisal might result in higher rates or even denial of the refinance application.

What should I do if my appraisal comes in low?

If your appraisal is lower than expected, you can request a reconsideration by providing additional comps or pointing out errors. Alternatively, you might need to make improvements to increase value or adjust your refinance or sale plans accordingly.

Are appraisals required for all home sales?

Not always. Cash sales might not require an appraisal, but most mortgage lenders do require one to protect their investment. It’s a standard part of financed real estate transactions.

How can I increase my mobile home’s appraisal value?

To boost your mobile home’s value, focus on maintenance, upgrades like new skirting or roofing, and ensuring it’s on a solid foundation. Also, consider the community amenities if it’s in a park, as these can positively influence appraisals.